Thoughts On Bank Runs, Dropping Rates, And Then Some.

This past week has been quite turbulent for us all. We witnessed two major bank failures with Silicon Valley Bank and Signature Bank, along with several large regional banks, such as First Republic, suffering a massive loss of market value. Internationally, Credit Suisse faced challenges due to fears of contagion spreading to systemically important banks.

Concerns persisted throughout the week despite numerous efforts. These included government guarantees for the depositors of SVB and Signature Bank, an additional big facility to backstop US banks, the injection of $30 billion deposits by a group of large US banks into First Republic, and finally, the National Bank of Switzerland stepping in for Credit Suisse. This crisis of confidence stems from years of a zero-rate lending environment that encouraged banks to purchase longer-dated bonds and Treasuries, as well as to hold longer-dated mortgages and bank-originated loans on their balance sheets in pursuit of higher yields. As the Fed increased rates significantly, the value of these loans decreased, resulting in potential “run on the bank” risks.

It’s crucial to note that the current mark-to-market issue is different from the 2008 crisis. In 2008, the issue was with poorly underwritten mortgages that became worthless when real estate prices stopped rising. Today, banks hold more capital in reserves, which can help cushion the blow to their balance sheets. Although the situation is stressful, it’s likely that the Fed and Treasury will find a way to calm the markets in the coming days. However, there is always the tail risk of an unknown factor creating a more significant problem.

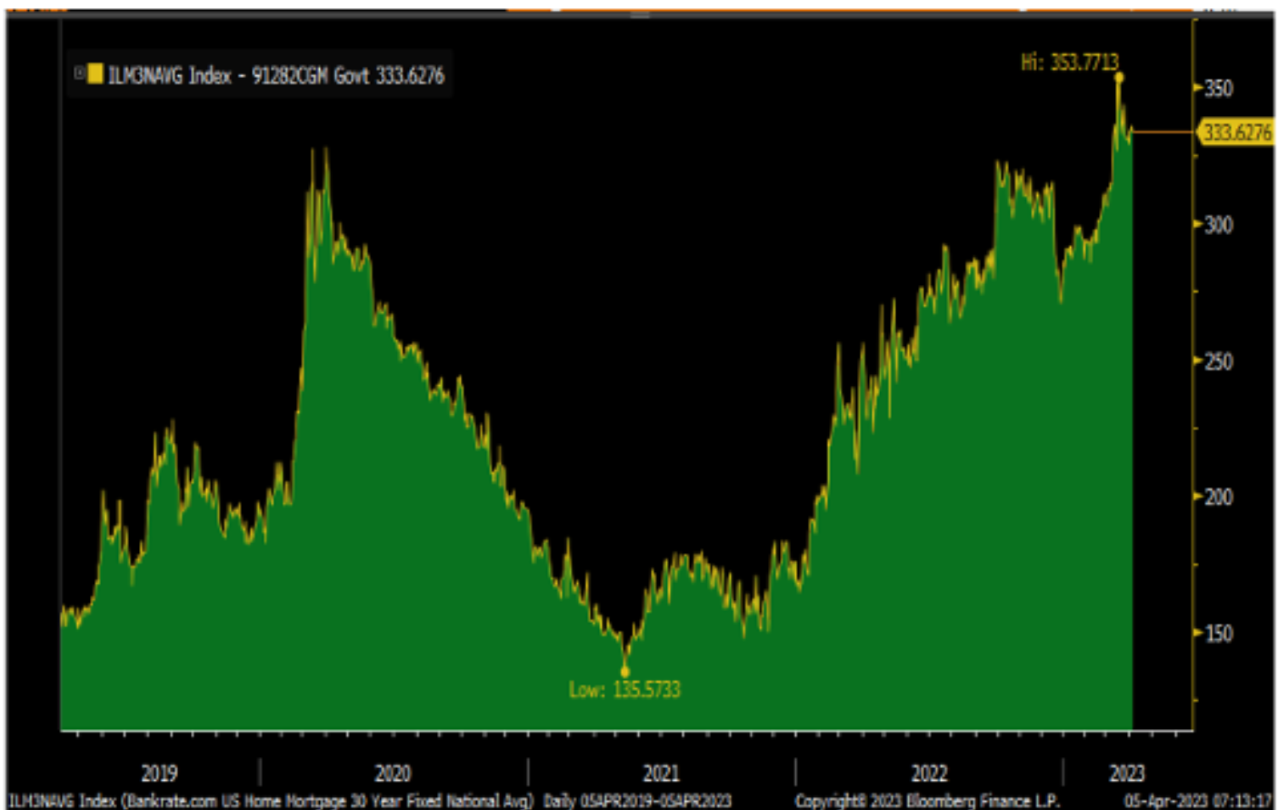

This banking debacle has implications for everyone in the real estate business, including realtors, mortgage bankers and brokers, escrow, and title companies. The decrease in confidence will likely hurt spending, delay house-hunting, and put additional pressure on sellers to lower prices. The drop in interest rates, now below the mid-5% range for most lending products, might provide some relief as banks tighten lending standards. Nonetheless, confidence has been hit hard. We suspect potential buyers to enter the market very cautiously for some time, even after equity and bond markets settle down.

The shrinking yield curve inversion has increased the probability of a recession. Historically, the unwinding of the inversion signals a higher probability of recession. The decisions of the Federal Reserve and European Central Bank regarding interest rates will further impact the global marketplace. How these institutions will balance market stabilization and inflation control remains to be seen.

Mortgage Brokers In The Current Market

Seasoned mortgage brokers are poised to play an essential role amidst the shift in the financial landscape last week. Numerous lesser-known lenders offer competitive rates, common-sense underwriting, and reasonable depository requests (at FDIC limits) as part of their portfolio product offerings. From complex full-doc loans to loans with as little as 5% down up to $1.5 million, and even stated income loans, these products are provided by regulated institutions. They are often priced better than those offered by large mortgage bankers. At Insignia Mortgage, we have experienced a significant uptick in loan requests, as borrowers seek these products without needing to transfer a substantial portion of their personal or business assets.