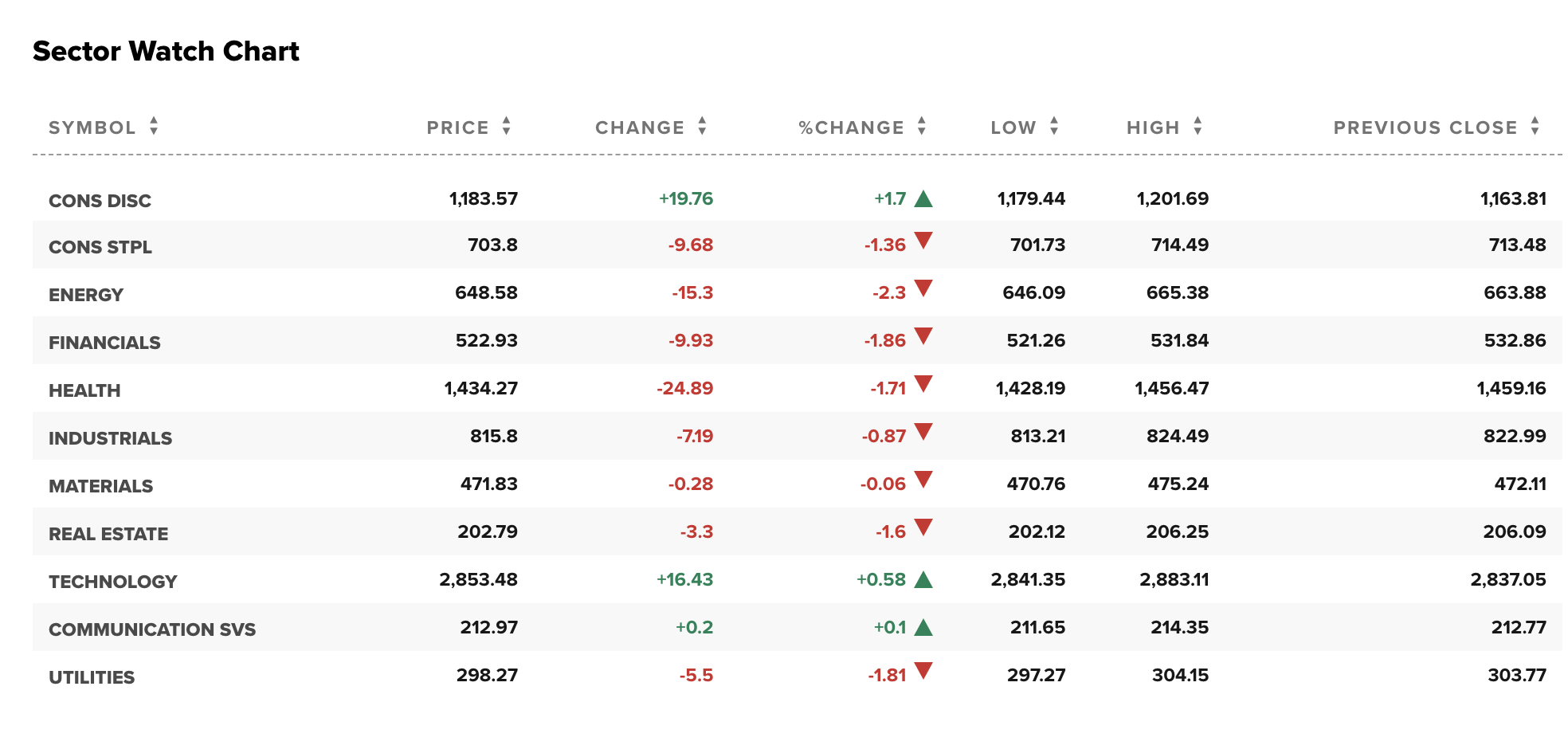

December Jobs Report Keeps Rates Flat

A better-than-expected Jobs Report pushed interest rates above 4% this morning before retreating down. A deeper dive into the Jobs Report suggests the jobs market may be cooling off. With a drop in the participation rate, more temp workers are unable to find jobs and more people accepting part-time work or working fewer hours. Employers remain cautious about firing workers given the difficulty experienced in replacing those workers during COVID and post-COVID. Of additional concern is wage growth, which is still running at 4% plus, a number higher than the Fed would like to see. On Wall Street, some believe the report was good enough to keep the Fed on pause through at least March, perhaps even longer.

Inflation has cooled on the goods front, but wage and service inflation are still too high. Geopolitical worries abound including the Israel-Palestine conflict, which is starting to create issues with major shipping vessels navigating the Strait of Hormuz, causing a rise in shipping costs and potentially oil prices. The worry here is that one wrong move could spark a regional war which could have unintended consequences, including an oil spike, which could complicate the Fed’s inflation fight. However, that is an obvious problem so the markets may have already priced in this outcome. One never does know.

We have spoken previously about the path to 5% mortgage rates and we are getting closer. One requirement to reaching this goal is that the mortgage spreads over Treasuries must continue to compress. The Wall Street Journal reported today that this is finally happening, with the expectation that should Treasury rates fall further, the mortgage spread would also follow.

A big reason spreads have been so wide is that banks and investors have been concerned about a drop in interest rates and the refinance risk associated with those drops. With the quick decline from 5% to 4% in the 10-year treasury, lenders are starting to get more competitive on pricing. In addition, another tailwind for real estate brokers and mortgage originators alike is the start of a new year and new volume targets so pricing remains sharp, which has led to much-improved activity to establish the year.

A quick look at programs and types of borrowers

- High Net worth with banking:

- Rates from 5.250%/6.196% APR. Loan amounts up to $25M

- Complex high net worth with banking:

- Rates from 6.000%/6.488%. Loan amounts to $10M

- Traditional Jumbo:

- Rates from 6.000%/6.488%. Loan amounts to $4M

- No Income Verification Loans:

- Rates from 7.500%/7.603%. Loan amounts up to $2.5M

- Conforming Loans:

- Rates from 5.875%/6.032%. Loan amounts up to $1,149,825

Happy New Year!