Get fresh weekly insights on rate direction and financial news from Damon Germanides,

Insignia’s co-founder, with over 20 years experience in the California mortgage marketplace.

Insignia Mortgage co-founder Chris Furie was recently quoted in The Ankler’s article on the SpaceX IPO’s expected impact on Southern California real estate. “I believe it’s gonna have a huge effect on the real estate market. I think it’s really good for Southern California real estate,” he said.

Due in part to the continued migration of families displaced by the Palisades Fire, thousands of newly wealthy SpaceX employees and early investors are expected to increase demand for housing, placing upward pressure on home prices and intensifying competition. This is predicted to hit the housing market most particularly in the South Bay and Westside.

View our unique interest rates by clicking the link below.

Why the Future of Mortgage Origination May Belong to Construction Finance Specialists

The mortgage industry has undergone significant changes over the past several years. As interest rates normalized and traditional refinance volume declined, many mortgage professionals found themselves searching for new opportunities to grow their business.

According to Damon Germanides, co-founder of Insignia Mortgage, one of the most compelling opportunities may be hiding in plain sight: construction lending.

In a recent feature published by Mortgage Professional America (MPA), Damon explored how construction financing has evolved from a niche lending category into one of the most underserved—and potentially rewarding—segments of the mortgage market.

The Growing Demand for Construction Loans

America continues to face a well-documented housing supply shortage. At the same time, many homeowners are choosing to renovate, expand, rebuild, or construct custom homes rather than compete in an inventory-constrained housing market.

Yet obtaining construction financing remains challenging.

While private capital has become increasingly active in serving professional builders and developers, many traditional banks have significantly reduced their consumer construction lending programs. This has created a financing gap for:

High-net-worth borrowers

Self-employed professionals

Business owners

Investors

Borrowers with complex income structures

Homeowners seeking major renovations or ground-up construction financing

For qualified borrowers, finding a lender that understands both construction risk and non-traditional income documentation can be difficult.

Why Construction Lending Requires Specialized Expertise

Unlike conventional residential mortgages, construction loans require a deeper level of analysis and project evaluation.

Mortgage professionals must understand not only the borrower’s financial profile but also the viability of the project itself.

This includes reviewing:

Construction budgets

Contractor agreements

Architectural plans

Permits and approvals

Draw schedules

Project timelines

After-completion valuations

Exit strategies

Successfully navigating these factors requires a blend of real estate finance expertise, project analysis, and risk management.

As a result, construction lending has become a specialization that many mortgage professionals avoid—but one that can create substantial value for clients.

Construction Lending and the Rise of Non-QM Solutions

One of the most exciting developments in today’s market is the growing intersection between construction lending and Non-QM mortgage products.

Historically, many self-employed borrowers struggled to qualify for construction financing because traditional underwriting relied heavily on tax returns that often failed to reflect actual cash flow.

Emerging alternatives—including bank statement loan programs and other Non-QM solutions—are beginning to create new pathways for borrowers who have strong financial profiles but unconventional documentation.

This trend has the potential to expand access to construction financing while giving mortgage professionals more tools to serve complex borrowers.

Why Construction Financing Can Help Mortgage Brokers Grow

Market cycles reward adaptability.

Mortgage professionals who develop expertise in construction lending, bridge financing, mixed-use properties, and small-balance commercial transactions often find themselves less dependent on traditional purchase and refinance volume.

Construction lending offers several advantages:

Strong Referral Opportunities

Builders, architects, contractors, developers, real estate professionals, and satisfied borrowers frequently become repeat referral sources.

Higher Barriers to Entry

The complexity of construction lending creates a competitive advantage for brokers willing to invest in learning the space.

Long-Term Client Relationships

Construction projects often span months or years, creating opportunities to build deeper relationships with clients.

Diversified Revenue Streams

Construction loans can complement traditional residential mortgage origination and help smooth volume fluctuations during market transitions.

The Future of Construction Lending

As housing supply challenges continue, demand for renovation financing, custom home construction loans, and ground-up development financing is expected to remain strong.

At the same time, private lenders, Non-QM lenders, and specialized mortgage professionals are increasingly filling the gaps left by traditional institutions.

For mortgage brokers, the opportunity is clear: developing expertise in construction finance today may create a sustainable competitive advantage for years to come.

Partner With Construction Lending Experts

At Insignia Mortgage, we specialize in helping borrowers navigate complex financing scenarios, including:

Construction Loans

Ground-Up Development Financing

Bridge Loans

Non-QM Mortgages

Jumbo & Super Jumbo Loans

Bank Statement Loans

Investor Financing

Luxury Real Estate Lending

Whether you’re building a custom home, renovating an existing property, or exploring creative financing options, our team has the experience and relationships needed to help structure a successful solution.

Learn More

Read Damon Germanides’ full feature in Mortgage Professional America, “Construction Lending Is Where Brokers Either Grow or Get Left Behind” here.

Contact Insignia Mortgage today to discuss your construction financing needs and explore the lending solutions available in today’s evolving market.

At Insignia Mortgage, we specialize in helping borrowers navigate complex mortgage scenarios that often require more than a conventional lending approach.

In Q1 2026, our team successfully funded a sampling of notable loan transactions across California and Florida, including high-LTV financing, jumbo mortgage solutions, bank statement loans, cross-collateralization strategies, bridge financing, and tailored loan structures for borrowers with unique income or asset profiles.

These transactions reflect the strength of Insignia Mortgage’s experience, lender relationships, and ability to structure mortgage solutions for clients whose financial circumstances may not fit within a standard lending box.

Notable Q1 2026 Funded Transactions

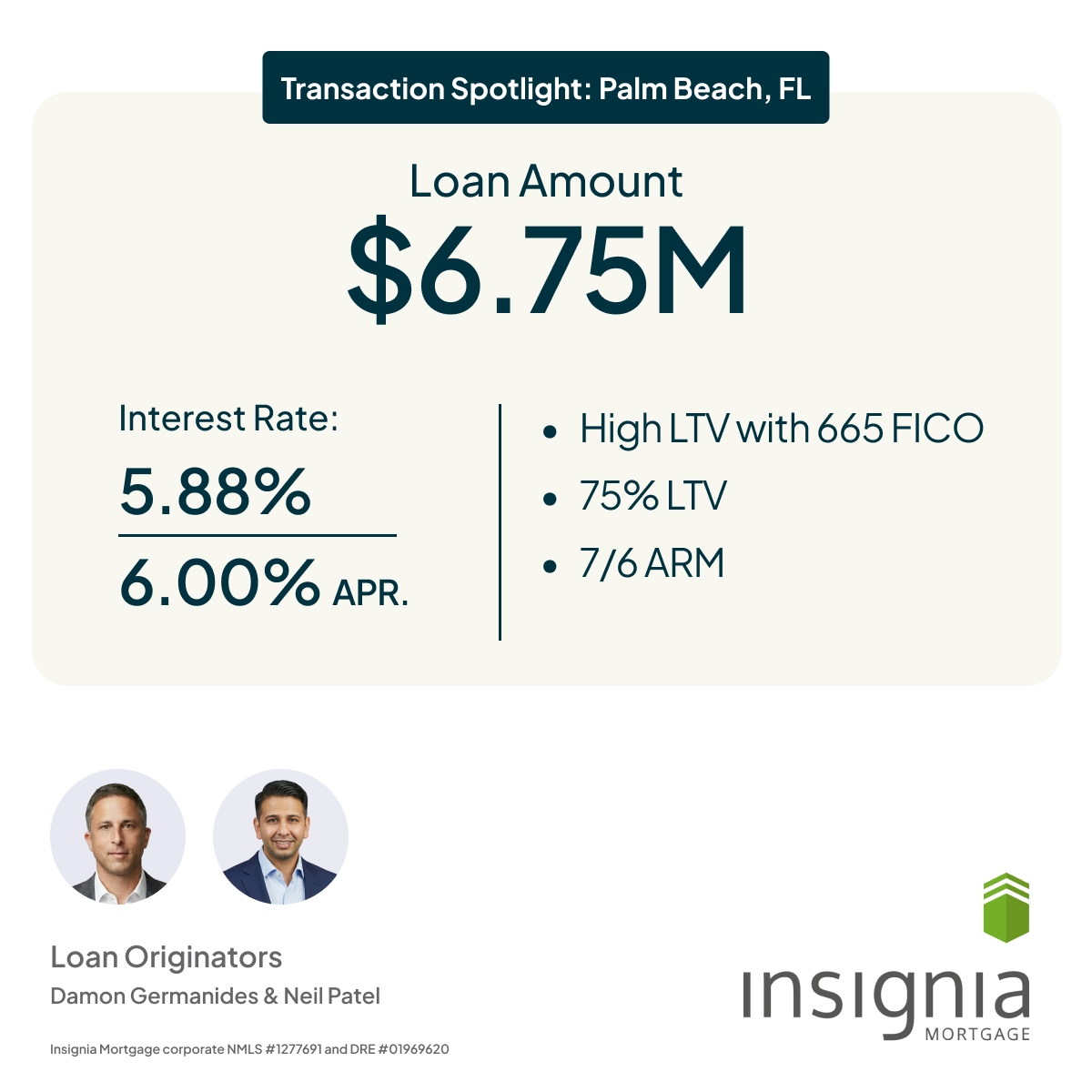

Palm Beach, Florida: $6.75M High-LTV Jumbo Loan

Insignia Mortgage funded a $6.75 million loan in Palm Beach, Florida, structured as a 7/6 ARM with 75% loan-to-value.

This transaction involved a high-LTV scenario with a 665 FICO score, requiring careful lender placement and structuring. The loan was originated by Damon Germanides and Neil Patel.

Loan Highlights:

Detail

Transaction Information

Location

Palm Beach, FL

Loan Amount

$6.75M

Interest Rate

5.88%

APR

6.00%

LTV

75%

Loan Type

7/6 ARM

Scenario

High LTV with 665 FICO

This transaction demonstrates how experienced mortgage advisors can help qualified borrowers explore options even when the scenario includes credit or leverage considerations that require a more customized lending approach.

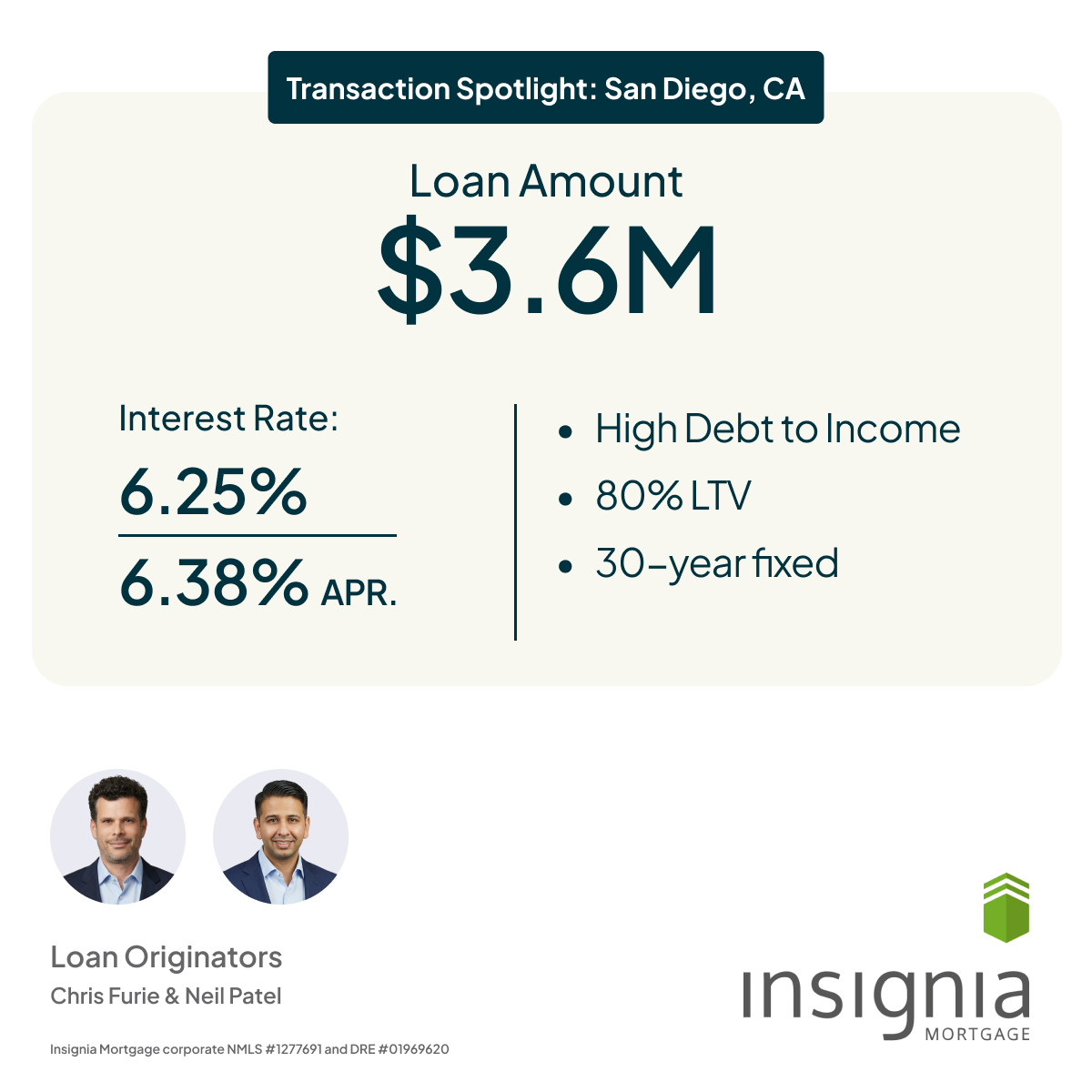

San Diego, California: $3.6M High-Debt-to-Income Loan

In San Diego, California, Insignia Mortgage funded a $3.6 million loan structured as a 30-year fixed mortgage with 80% loan-to-value.

This transaction involved a borrower with a high debt-to-income profile, a common challenge for high-net-worth individuals, business owners, investors, or borrowers with complex financial structures. The loan was originated by Chris Furie and Neil Patel.

Loan Highlights:

Detail

Transaction Information

Location

San Diego, CA

Loan Amount

$3.6M

Interest Rate

6.25%

APR

6.38%

LTV

80%

Loan Type

30-Year Fixed

Scenario

High Debt-to-Income

For borrowers with elevated debt-to-income ratios, access to the right lending partners can make a significant difference. Insignia Mortgage works to identify solutions that account for the full financial picture, rather than relying solely on one traditional metric.

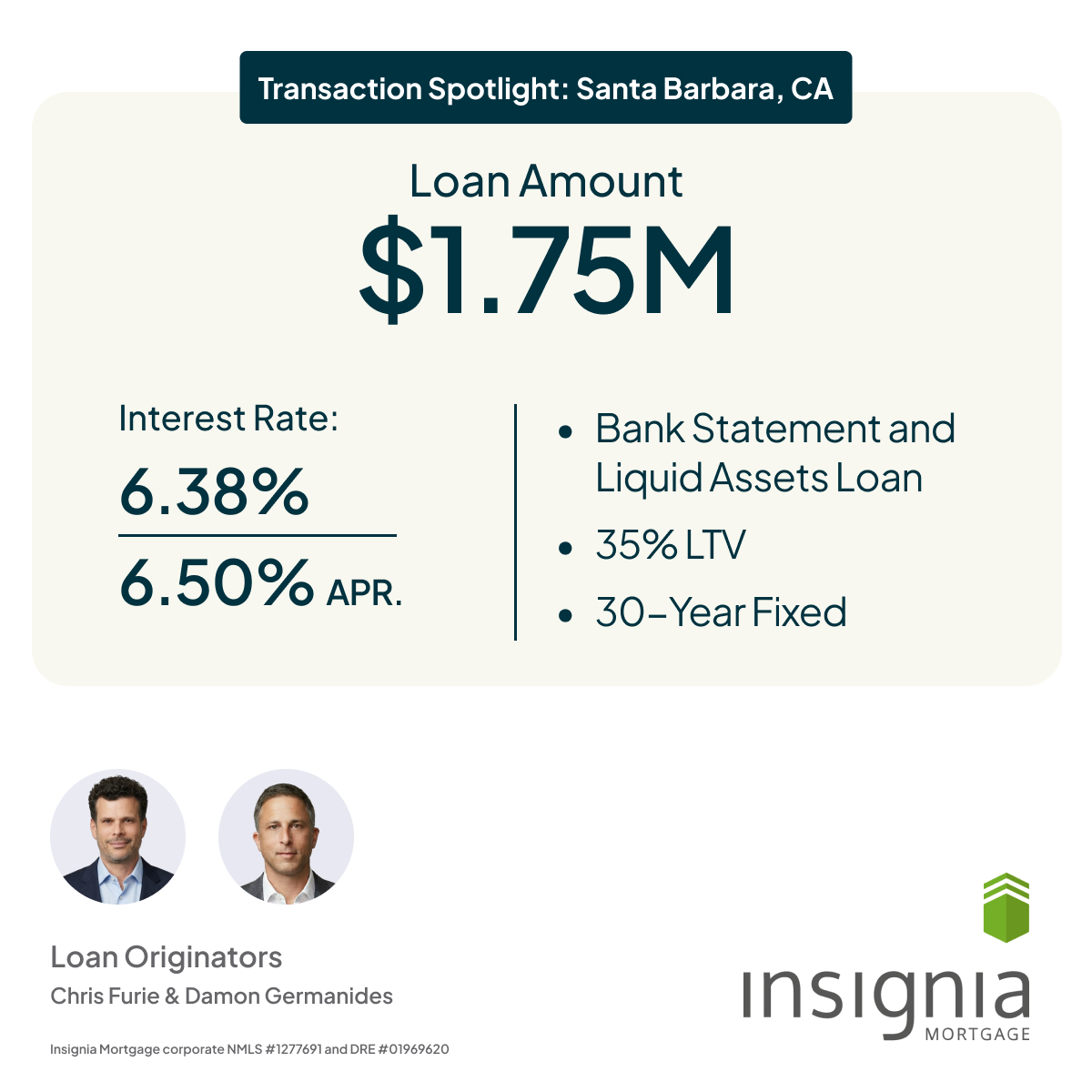

Santa Barbara, California: $1.75M Bank Statement and Liquid Assets Loan

Insignia Mortgage funded a $1.75 million loan in Santa Barbara, California, using a bank statement and liquid assets loan structure.

The loan was structured as a 30-year fixed mortgage with 35% LTV, originated by Chris Furie and Damon Germanides.

Loan Highlights:

Detail

Transaction Information

Location

Santa Barbara, CA

Loan Amount

$1.75M

Interest Rate

6.38%

APR

6.50%

LTV

35%

Loan Type

30-Year Fixed

Scenario

Bank Statement and Liquid Assets Loan

Bank statement and asset-based mortgage programs can be valuable options for self-employed borrowers, business owners, entrepreneurs, and high-net-worth individuals who may have strong liquidity but nontraditional income documentation.

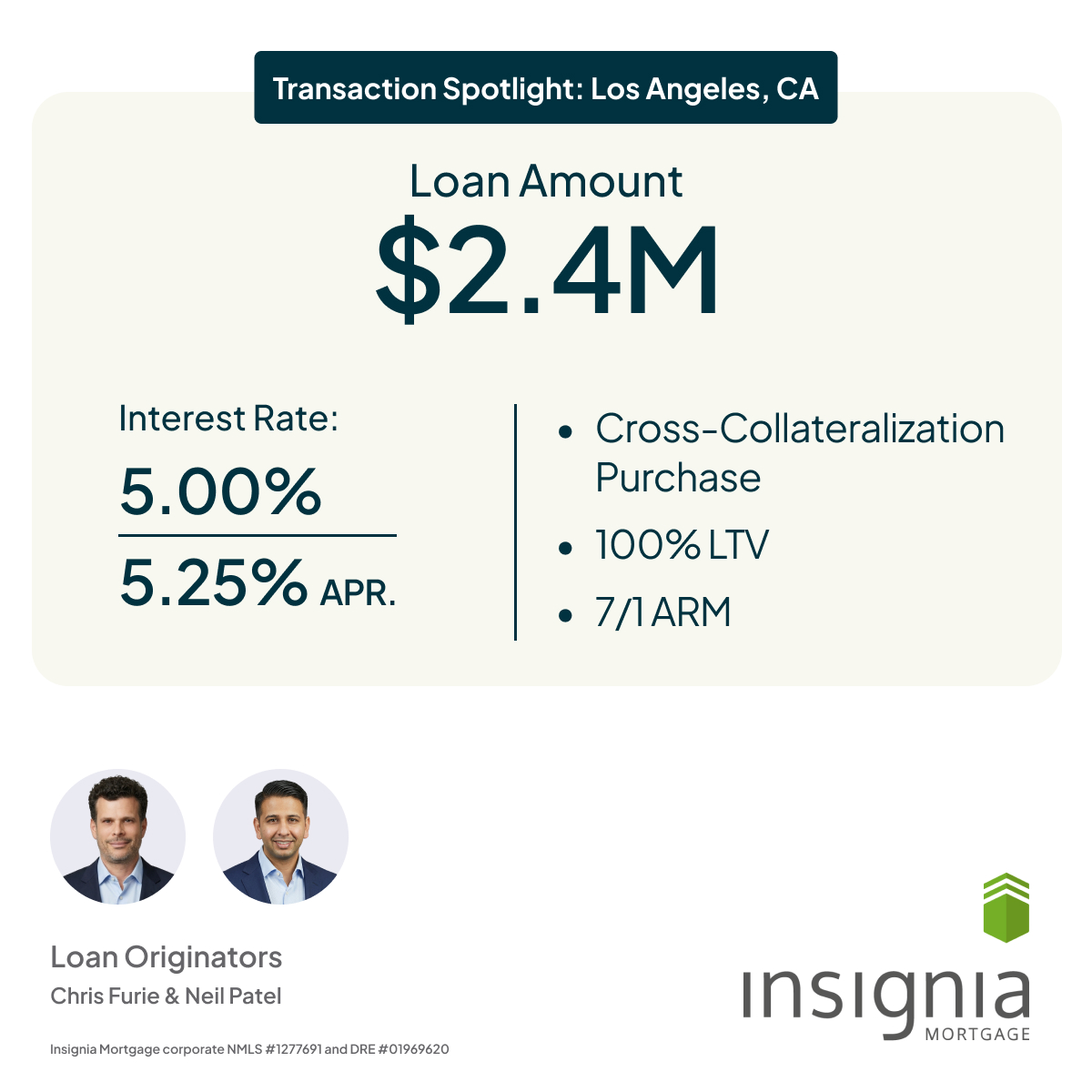

Los Angeles, California: $2.4M Cross-Collateralization Purchase

In Los Angeles, California, Insignia Mortgage funded a $2.4 million cross-collateralization purchase loan structured as a 7/1 ARM.

This transaction featured 100% LTV, requiring a specialized approach to collateral, risk, and lending structure. The loan was originated by Chris Furie and Neil Patel.

Loan Highlights:

Detail

Transaction Information

Location

Los Angeles, CA

Loan Amount

$2.4M

Interest Rate

5.00%

APR

5.25%

LTV

100%

Loan Type

7/1 ARM

Scenario

Cross-Collateralization Purchase

Cross-collateralization can be a strategic financing tool for borrowers who own additional real estate or assets and want to structure financing around a broader collateral position.

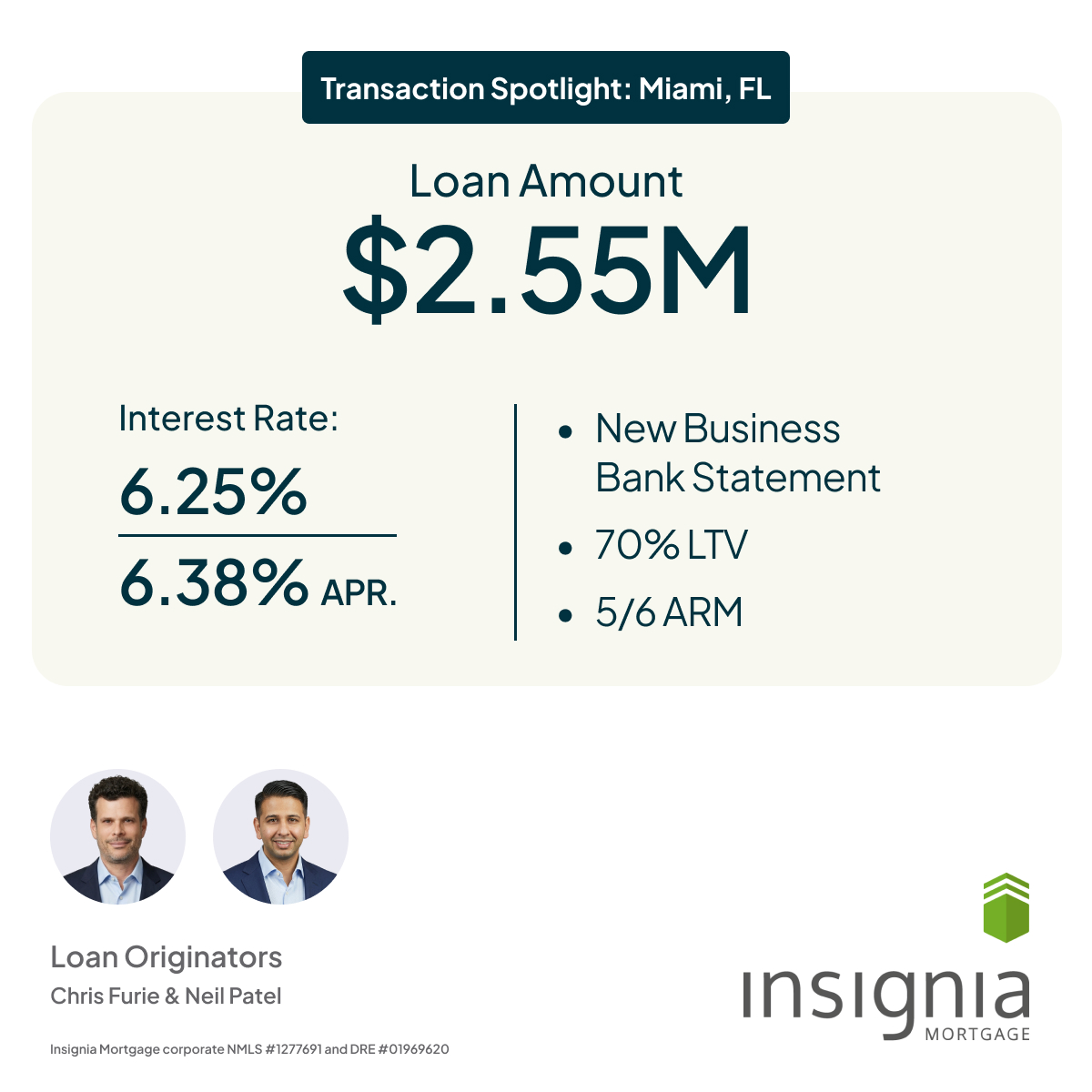

Miami, Florida: $2.55M New Business Bank Statement Loan

Insignia Mortgage funded a $2.55 million loan in Miami, Florida, structured as a 5/6 ARM with 70% LTV.

This transaction involved a new business bank statement scenario, requiring a lending solution that accounted for nontraditional income documentation. The loan was originated by Chris Furie and Neil Patel.

Loan Highlights:

Detail

Transaction Information

Location

Miami, FL

Loan Amount

$2.55M

Interest Rate

6.25%

APR

6.38%

LTV

70%

Loan Type

5/6 ARM

Scenario

New Business Bank Statement

For newer business owners, traditional income verification can be challenging. Bank statement loan programs may provide an alternative path for borrowers who can demonstrate cash flow through business or personal bank deposits.

Long Beach, California: $3.16M Cross-Collateralization Bridge Loan

In Long Beach, California, Insignia Mortgage funded a $3.16 million bridge loan with a 12-month term and 50% LTV.

This transaction used a cross-collateralization bridge structure, originated by Damon Germanides.

Loan Highlights:

Detail

Transaction Information

Location

Long Beach, CA

Loan Amount

$3.16M

Interest Rate

9.625%

LTV

50%

Loan Type

Bridge Loan

Term

12 Months

Scenario

Cross-Collateralization Bridge

Bridge financing can be useful when borrowers need short-term capital to complete a purchase, reposition assets, unlock liquidity, or manage timing between transactions.

What These Transactions Say About Today’s Mortgage Market

The Q1 2026 funded transactions highlight a key trend in the luxury and complex mortgage market: borrowers often need financing solutions that go beyond conventional underwriting.

Many affluent borrowers, business owners, real estate investors, and self-employed professionals have strong financial profiles, but their income, assets, or collateral may not fit neatly into traditional loan guidelines.

That is where Insignia Mortgage’s expertise becomes valuable.

Our team regularly helps clients evaluate options such as:

Jumbo mortgage financing High-LTV loan structures Bank statement mortgage programs Asset-based lending solutions Cross-collateralized financing Bridge loans Adjustable-rate mortgage options Complex income documentation scenarios Loans for self-employed borrowers and business owners

Frequently Asked Questions About Complex Mortgage Scenarios

What is a jumbo mortgage?

A jumbo mortgage is a home loan that exceeds the conforming loan limits set for conventional mortgages. Jumbo loans are commonly used for luxury properties, high-cost markets, and larger loan amounts.

What is a bank statement mortgage?

A bank statement mortgage allows eligible borrowers to use bank statements as part of the income documentation process. This can be especially useful for self-employed borrowers, business owners, and entrepreneurs whose tax returns may not fully reflect their cash flow.

What does high LTV mean?

LTV stands for loan-to-value. A high-LTV loan means the borrower is financing a larger percentage of the property’s value. High-LTV financing may require stronger compensating factors, such as liquidity, credit history, reserves, or additional collateral.

What is cross-collateralization?

Cross-collateralization is a lending strategy where more than one asset or property may be used to support a loan. This can help borrowers structure financing in situations where traditional collateral or down payment structures may not be ideal.

What is a bridge loan?

A bridge loan is a short-term financing solution often used to help borrowers bridge the gap between transactions. It may be used when purchasing a new property before selling an existing one, accessing temporary liquidity, or managing timing-sensitive real estate opportunities.

Work With a Mortgage Team Experienced in Complex Lending

Insignia Mortgage has built its reputation on helping clients solve complex lending scenarios with precision, creativity, and discretion.

Whether you are purchasing a luxury property, refinancing a jumbo mortgage, seeking a bank statement loan, exploring asset-based lending, or evaluating a bridge financing strategy, our team can help identify the right path forward.

Insignia Mortgage is proud to announce that multiple members of our team have once again been recognized in Scotsman Guide’s 2026 Top Originators Rankings, including strong national placements in the publication’s highly respected Top Mortgage Brokers category. This year’s rankings highlight the strength of the Insignia Mortgage team across both overall loan production and broker-specific performance.

2026 Scotsman Guide Rankings for Insignia Mortgage Include:

Damon Germanides — #60 in Total Dollar Volume | #10 in Top Broker Rankings

Chris Furie — #168 in Total Dollar Volume | #22 in Top Broker Rankings

Neil Patel — #1753 in Total Dollar Volume | #145 in Top Broker Rankings

For Insignia Mortgage, this recognition reflects more than just annual production. It reinforces what clients, referral partners, and industry peers already know: Insignia Mortgage is one of the nation’s standout boutique mortgage brokerages for jumbo, non-QM, and complex financing solutions.

Why the Top Mortgage Brokers Ranking Matters

While overall loan volume is an important benchmark, the Top Mortgage Brokers category is especially meaningful for the team. This category reflects performance specifically within the mortgage broker channel — a segment of the lending market that often requires more strategy, more lender access, and more flexibility than traditional bank or retail lending.

For borrowers, this matters because our mortgage brokers can provide:

broader access to lending options

more customized loan structures

greater flexibility for complex borrower scenarios

specialized solutions for jumbo and non-QM financing

more personalized support throughout the loan process

In higher-value and more financially nuanced markets, those advantages make a major difference. That is why having three Insignia Mortgage professionals ranked nationally in Top Broker Rankings is such a strong signal of expertise and market leadership.

Damon Germanides — Ranked #10 in Top Mortgage Brokers

Insignia Mortgage co-founder Damon Germanides earned one of the highest broker rankings in the country, coming in at #10 nationally in Top Broker Rankings, in addition to being ranked #60 in Total Dollar Volume.

This recognition reinforces Damon’s position as one of the top-performing mortgage brokers in the country, reflecting years of success helping clients secure financing in complex and high-value lending scenarios. As a leader at Insignia Mortgage, Damon has built a reputation for structuring loans for borrowers who often fall outside standard retail bank lending models, including self-employed borrowers, high-net-worth individuals, real estate investors, and clients with more sophisticated financial profiles.

Chris Furie — Ranked #22 in Top Mortgage Brokers

Insignia’s other co-founder Chris Furie also earned strong national recognition, ranking #22 in Top Broker Rankings and #168 in Total Dollar Volume.

Chris’s placement highlights not only strong production but also his effectiveness as a mortgage broker operating in a market where thoughtful loan strategy and lender access are essential. Known for his ability to help borrowers navigate nuanced financial scenarios, Chris has played an important role in building Insignia Mortgage’s reputation as a brokerage that delivers results where standard lending channels often fall short.

Neil Patel — Ranked #145 in Top Mortgage Brokers

Licensed California CPA and long-time Insignia Mortgage rockstar broker Neil Patel rounded out the team’s Scotsman Guide recognition, ranking #145 in Top Broker Rankings and #1753 in Total Dollar Volume.

Neil’s recognition reflects the depth and continued growth of the Insignia Mortgage platform. His contribution shows that Insignia’s success is not limited to one individual but supported by a broader team of mortgage professionals capable of delivering results at a national level.

Together, these rankings reflect the collective strength of the Insignia Mortgage team and the value of its broker-led approach.

What These Rankings Say About Insignia Mortgage

Having three nationally ranked mortgage brokers on the same team is a meaningful distinction.

It signals that Insignia Mortgage is not simply a high-volume lender — it is a brokerage with a proven ability to deliver strategic financing solutions in a highly competitive and increasingly complex mortgage environment.

This is especially important for borrowers who need financing beyond standard conventional lending options.

Insignia Mortgage specializes in helping clients with:

In many cases, the difference between a difficult loan and a successful close comes down to experience, lender relationships, and structuring expertise — all core strengths of the mortgage broker model.

Why Boutique Mortgage Brokerages Continue to Stand Out

The modern mortgage market is increasingly shaped by borrowers who need more than a standard rate quote. Many clients today have financial profiles that include:

business ownership

multiple entities or income streams

trust or investment income

variable tax returns

significant assets with non-traditional documentation

higher loan amounts or luxury property purchases

For these borrowers, a boutique mortgage broker often offers significant advantages over a one-size-fits-all lending experience.

Benefits of working with an Insignia Mortgage broker:

access to a wider network of lenders

more flexible underwriting options

more strategic loan matching

customized solutions for complex scenarios

more hands-on communication and execution

That is where Insignia Mortgage has built its brand — and why recognition in the Top Mortgage Brokers rankings is especially relevant.

A Longstanding Presence on the Scotsman Guide Rankings

One of the most important parts of this recognition is not just this year’s placements — it is the consistency behind them.

Insignia Mortgage has maintained a longstanding presence on the Scotsman Guide rankings throughout the years, reflecting the kind of repeat performance that is difficult to sustain in a constantly changing lending market.

That consistency matters because mortgage lending is cyclical.

Brokerages that continue to perform and remain nationally recognized through those shifts are often the ones with the strongest operational discipline, borrower trust, and lender access. That long-term consistency is part of what has made Insignia Mortgage a respected name in the mortgage and real estate finance space.

What This Means for Borrowers and Referral Partners

For borrowers and referral partners, these rankings offer more than just industry recognition — they provide confidence.

When working with a mortgage broker, clients want to know they are partnering with professionals who can:

solve problems creatively

communicate clearly

structure loans intelligently

move with urgency

and close reliably

That is especially important for:

luxury home buyers

self-employed borrowers

business owners

investors

real estate agents

attorneys

CPAs

wealth advisors

and clients with complex mortgage needs

Insignia Mortgage’s continued recognition in Scotsman Guide reflects exactly that type of value.

Work With a Nationally Ranked Mortgage Broker

If you are exploring financing options and want to work with a team recognized among the nation’s top mortgage brokers, Insignia Mortgage is here to help.

Whether you are:

purchasing a high-value property

refinancing an existing mortgage

exploring non-QM financing

structuring a jumbo loan

or navigating a more complex borrower profile

Insignia Mortgage offers the expertise and lending access to help guide the process strategically.

Contact Insignia Mortgage

To learn more about available loan programs, mortgage options, or financing strategies, connect with our team here.

The mortgage industry continues to evolve rapidly in 2026. From advances in artificial intelligence to shifting interest rate expectations and tighter housing supply, brokers and borrowers alike are navigating a more complex lending environment.

Recently, Damon Germanides, Co-Founder of Insignia Mortgage, joined the Broker Intel panel hosted by Mortgage Professional America to discuss what lenders and borrowers should expect in today’s market. The panel explored several key trends shaping mortgage lending today, including the growing role of AI, the outlook for interest rates, and the continued expansion of the mortgage broker channel.

Below are the major takeaways from the conversation.

1. Mortgage Market Activity Is Improving in 2026

After several challenging years for the housing market, early indicators in 2026 suggest improved activity. According to Damon, mortgage application volume has increased compared to previous quarters. This is driven in part by slightly improved interest rate conditions and renewed appetite from lenders.

However, one major constraint remains: housing supply.

Many borrowers are receiving loan approvals but struggling to secure homes due to limited inventory, particularly in entry-level and mid-tier markets. This imbalance between demand and supply continues to slow purchase conversions even as lending conditions improve.

For borrowers, this means preparation and strong financing strategies remain critical to maintain a competitive edge in today’s housing market.

2. The Mortgage Broker Channel Continues to Gain Market Share

Another important trend discussed during the panel was the continued growth of the mortgage broker channel. Mortgage brokers have progressively been able to offer competitive pricing compared with large retail banks by leveraging access to multiple lenders and loan products.

This flexibility allows brokers to:

Compare rates across multiple lending institutions

Structure more customized loan solutions

Move quickly when borrowers need approvals or adjustments

As a result, more borrowers and loan originators are shifting toward broker-based lending models. For clients working with experienced brokerage firms like Insignia Mortgage, this often translates to greater access to loan options and more competitive pricing.

3. AI Is Changing Mortgage Operations—But Not Relationships

Artificial intelligence is increasingly becoming part of mortgage origination workflows. During the panel discussion, Damon highlighted how technology and automation are helping loan teams manage tasks like follow-up, reminders, and lead tracking.

These tools can improve efficiency considerably, allowing loan officers to focus more time on advising clients and structuring deals rather than handling repetitive administrative tasks.

However, one message from the panel was clear:

AI is improving efficiency—but it cannot replace trusted mortgage advice.

Mortgage lending remains fundamentally relationship-driven. Borrowers still rely on experienced professionals to guide them through financing decisions, particularly for complex scenarios involving jumbo loans, investment properties, or construction financing.

4. HELOCs and Second Liens Are Growing in Popularity

Another notable trend discussed in the panel is the renewed interest in home equity products. With many homeowners locked into historically low first-mortgage rates from prior years, refinancing often does not make financial sense. Instead, borrowers are increasingly turning to:

HELOCs (Home Equity Lines of Credit)

Second lien loans

Business or unsecured credit lines

These financing options allow homeowners to access equity for investments, renovations, or liquidity without replacing their existing mortgage. For borrowers seeking flexibility, these products are becoming a valuable part of the lending landscape.

5. Interest Rates and the Federal Reserve Outlook

Interest rates remain one of the most important variables influencing the housing market. Panelists noted that the Federal Reserve has taken a cautious stance on rate changes due to persistent inflation pressures.

While markets anticipate potential policy shifts later in the year, the consensus view is that rates may stabilize rather than decline in the near term.

For borrowers, the key takeaway is that timing the market perfectly is difficult. Many experts emphasize that purchasing or refinancing decisions should focus on long-term financial goals rather than short-term rate speculation.

6. The Role of Technology in the Next Phase of Mortgage Lending

One of the most interesting themes from the panel was how automation is reshaping the operational side of mortgage lending. Technology platforms and AI tools are reducing the time required to originate loans and manage client communication. This shift allows brokerages to scale operations more efficiently and serve borrowers more effectively.

However, faster processes also introduce new challenges, including increased competition and pressure on margins across the lending industry. Mortgage companies that combine technology, expertise, and strong client relationships are likely to remain best positioned as the industry continues to evolve.

Main Takeaways For Borrowers

For borrowers and real estate investors, the insights from the Broker Intel panel highlight several important trends:

Mortgage markets are gradually stabilizing in 2026

Housing inventory remains one of the biggest obstacles for buyers

Mortgage brokers are gaining share due to flexibility and competitive pricing

AI is improving efficiency but not replacing expert loan guidance

Home equity products are becoming more widely used

Understanding these dynamics can help borrowers make more informed financing decisions in a rapidly changing market.

Watch the Full Interview

To hear the full discussion featuring Damon Germanides of Insignia Mortgage, watch the Broker Intel panel interview from Mortgage Professional America.

The mortgage industry enters 2026 with a familiar mix of pressure and possibility: affordability remains strained, inventory is tight, and regulation continues to evolve. In a recent Broker Intel discussion on MPA TV, the expert panelists agreed that brokers who pair technology-driven speed with real human guidance will continue winning market share.

Insignia Mortgage co-founder Damon Germanides joined Tom Wallace (Edge Home Finance) and Andrew Russell (RCG Mortgage) to discuss the current mortgage landscape and what originators should do next. Their conversation wasn’t theoretical. It was grounded in day-to-day reality. They provided perspective on situations where borrowers can’t find homes, how pre-approvals die on the vine, and the growing gap between “getting leads” and “closing clean.”

Below are the highlights of this expert talk and its impact on borrowers, real estate partners, and anyone looking for a smarter lending strategy in 2026.

1) AI is speeding up mortgages—but it’s not replacing the originator

The panel agreed: AI is changing the operating tempo of mortgage origination.

Tom Wallace described a world where underwriting capacity expands dramatically—underwriters who used to manage 20–30 files can now handle far more, and complex income scenarios can be evaluated faster. Now, loan officers get answers quicker, while borrowers and agents get clarity sooner.

Damon echoed the value of these tools, in particular the opportunity to shorten turn times, improve responsiveness to agents, and give borrowers more immediate feedback on qualification and options. He believes the right stack can “supercharge” brokers—but only if it’s designed for how originators actually work.

Andrew Russell brought the counterweight brokers need to hear: technology is not a substitute for business development and relationships. In his words, “he or she who makes the calls wins.” Especially in the purchase business, grit, communication, and trust still decide which offers get accepted and which lenders win referral loyalty.

Overall, AI is an advantage—but only when paired with strong execution and human credibility.

2) The purchase market is still a relationship game—especially in low inventory environments

When inventory is thin, being “good” isn’t enough. Andrew framed it like this: there are fewer “pies,” so you need a bigger share of the “slices.” His team leans into proactive listing-agent outreach—positioning their buyer as strong and emphasizing speed to close.

Inventory constraints make every transaction more competitive, especially this 2026. Borrowers aren’t just shopping for rates, they’re trying to win homes. Realtors aren’t just looking for pre-approvals—they’re looking for certainty, communication, and fast problem-solving- especially when a deal gets tight.

Moreover, Damon emphasized the fact that purchase transactions continue to rely on credible, real-time human conversation. AI may help with refi automation and internal efficiency, but on purchases, the buyer and listing side still want an originator who understands nuance, can anticipate issues, and can explain the “why” behind the numbers. In a tight market, brokers win by delivering confidence, speed, clarity, and expertise.

3) The biggest headwinds: affordability and inventory (and they’re hitting even high earners)

Damon’s commentary on affordability was one of the sharpest moments in the discussion—because it didn’t romanticize the market.

Insignia Mortgage operates heavily in major metros (including California), and Damon described a growing trend: pre-approvals that fall apart not because credit fails, but because reality strikes. Even when financing is possible, borrowers reach a point where the monthly stress becomes defeating.

He highlighted a dynamic that many high-income buyers experience in expensive markets: even households earning what most would consider “top-tier” incomes can still struggle to purchase a home without taking on a payment that consumes an uncomfortable share of their monthly cash flow.

What stood out most wasn’t just the market observation;it was the philosophy behind it:

Sometimes the best advice isn’t “yes.” It’s helping the borrower decide whether the deal actually makes sense for their life.

That’s a key element of Insignia’s positioning: complex lending is not just about approvals—it’s about advising intelligently when leverage and affordability collide. Affordability pressure isn’t just a loan problem—it’s a decision-quality problem. Great brokers help clients think clearly.

4) Broker retention is an underused growth lever (and a major industry weakness)

Tom Wallace made a strong point that many brokerages don’t want to confront: retention in the broker channel is low compared to other lending models.

His argument was not about blaming originators—it was strategic: if brokers could materially improve retention through better systems and outreach, they would create a major advantage, especially when market volume is harder to come by.

Damon’s earlier comments connect directly to this: the broker who is honest, consistent, and easy to work with becomes the person borrowers come back to—sometimes after another lender fails to deliver. Retention isn’t accidental. It’s built through process, communication, and trust—especially when the first deal is complex.

Damon outlined one of the biggest shifts in how he’s run Insignia over the past few years… When rate changes happened quickly, Insignia’s strong relationships with smaller banks and credit unions became a vulnerability—those institutions pulled back or hit capacity limits. That created a “double whammy” with rising rates and reduced lender availability.

Insignia’s response wasn’t panic. It was strategy.

They diversified capital sources and products so that business isn’t dependent on a narrow lender set.

They expanded into complementary solutions—Damon referenced building Insignia Capital Corp. as a bridge-lending platform to support developers and builders, while also creating a longer client lifecycle (bridge now, permanent financing later when stabilized).

Flexibility and innovation is key to success. The modern broker wins by being a solutions platform, not a single-lane lender.

6) Tech adoption must match the LO, not the other way around

Technology is only valuable if it becomes behavior, and behavior only changes when tools are intuitive. This was a very “real-world” point, and it matters for any growth-minded brokerage.

Damon noted that many successful originators are not technologists—and if the system is too complicated, it won’t be used. The goal is not “more tools.” The goal is better visibility and easier daily execution: dashboards, analytics, referral-source clarity, and action prompts that help LOs know where to focus.

7) 2026 outlook: don’t wait for rates to save you—build like it’s still hard

Overall, everyone agreed that 2026 will reward brokers who combine modern outreach with old-school competence.

Damon’s 2026 forecast summary:

He’s not assuming rates will be a tailwind.

If they improve, great—but brokers should prepare as if they won’t.

The brokers who commit through challenging conditions build their reputations, develop niches, and “plant seeds” that pay off later.

Andrew’s 2026 perspective summarized as a two-part operating system:

What you do when the phone rings (process, execution, tech, follow-through)

What you do to make the phone ring (marketing, business development, relationships, education content)

Tom’s 2026 forecast:

Tom shared his belief that the 2026 broker is competing in a world where social and digital education matter more than traditional media. He emphasized that the originators who can teach clearly will win attention and trust at scale.

What does this mean for borrowers and partners working with Insignia Mortgage?

If you’re a borrower, investor, or real estate partner navigating 2026, the MPA TV discussion reinforces what Insignia Mortgage is built for:

Complex files that require real underwriting intelligence

Speed and execution when timelines are tight

Honest guidance when affordability and leverage need to be balanced

Creative lending options, including jumbo, non-agency strategies, and bridge-to-perm pathways

A team led by professionals who understand that mortgage decisions are not just transactions—they’re long-term financial commitments

Damon’s approach to lending leadership is clear: use technology to move faster, but never replace the human expertise that wins purchases and builds trust. In a market where many deals die from uncertainty, that combination is exactly what clients and partners need.

If you’re planning a purchase, refinance, investment, or construction-related financing strategy in 2026, connect with the Insignia Mortgage team and explore options designed around your real-world scenario—not a one-size-fits-all box. Connect with our team today by clickinghere.

References:

Germanides, Damon. “Experts give their thoughts on navigating challenges to find success in 2026.” Mortgage Professional America, Jan. 7, 2026. (Mortgage Professional)

“Damon Germanides.” Mortgage Professional America (Broker Intel profile). Accessed Jan. 8, 2026. (Mortgage Professional)

2025 was a defining year for the Insignia Mortgage team, with a total loan volume of $415M closed. Across super jumbo purchases, high-LTV refinances, time-sensitive investment acquisitions, and complex borrower profiles, our team consistently delivered outcomes that many lenders considered impossible.

From borrowers putting just 20% down on super jumbo loans, to first-time U.S. earners qualifying without FICO scores or tax returns, to 21-day closes on investment properties—Insignia Mortgage proved why we are trusted for complex, high-stakes financing. Below is a look at our most impactful funded loans of 2025, capped by our December case study—and what this momentum means for clients heading into 2026.

Top Funded Loans of 2025: A Year of Complex Wins

$8.395M Super Jumbo Loan at 80% LTV – Los Angeles, CA

Borrower Need: A high-income client purchasing a primary residence wanted to limit their down payment to 20%—a major challenge in the super jumbo space. Insignia Solution:Damon Germanides sourced the only lender willing to offer 80% LTV on a super jumbo loan, paired with a competitive 7/1 ARM at 5.41% (5.63% APR). Result: The borrower secured their home with the leverage they wanted—without sacrificing pricing or structure.

$3.45M New U.S. Income Jumbo Loan – Los Angeles, CA

Borrower Need: A client new to the U.S. with no FICO score or tax returns needed jumbo financing—fast. Insignia Solution: Damon Germanides and Neil Patel identified a lender willing to qualify the borrower using newly established U.S. income, offering rates comparable to domestic borrowers. Result: The loan closed in under 30 days, removing a major barrier for international and relocating buyers.

$3.5M Refinance Using New Bonus Income – Los Angeles

A borrower facing an ARM adjustment had recently started a new role with compensation heavily weighted toward bonuses. Insignia structured a refinance using the new bonus income, stabilizing the loan and future cash flow.

$2.75M No-Income-Verification Purchase – Santa Barbara

Without selling an existing residence or providing income documentation, this borrower still needed to purchase a new home. Insignia sourced a bank that required no tax returns and no income verification, enabling a smooth closing.

$7.5M Investment Property Closed in 21 Days – Los Angeles

In the middle of a 1031 Exchange, timing was everything. Insignia matched the borrower with a lender that understood complex income and moved quickly—closing in just 21 days so the deal could move forward.

$8M High-LTV Jumbo Loan at 80% – Los Angeles

When a client needed maximum leverage on a jumbo purchase, Insignia delivered 80% financing with an interest-only ARM—closed in under 30 days despite tight underwriting requirements.

$2M Apartment Loan with Fast Close – Glendale

After inspections were complete, the borrower needed to close on a multifamily property in under 30 days. Insignia delivered both speed and pricing, securing the deal on time.

$1.565M 8-Unit Permanent Cash-Out Refinance – Los Angeles

Following a bridge loan used to renovate and stabilize an 8-unit property, Insignia Mortgage stepped in to secure permanent financing. The loan closed in 45 days, paid off bridge debt, and delivered additional cash-out proceeds with a flexible prepay structure.

$1.242M Agency Conforming Investment Purchase – Los Angeles

After being turned down by three banks due to debt-ratio concerns, Insignia underwriters re-evaluated business and personal returns—closing the deal five days before COE and keeping ratios within agency guidelines.

Why 2026 Is the Best Time to Work with Insignia Mortgage

The results of 2025 weren’t accidental—they were built on deep lender relationships, elite underwriting expertise, and a relentless focus on borrower strategy. As we move into 2026, Insignia Mortgage is expanding access to:

Higher-LTV jumbo and super jumbo solutions

Foreign national and new-to-U.S. income programs

No-income and asset-based lending

Accelerated closings for competitive purchases

Creative structures for investors, 1031 exchanges, and multifamily assets

Whether you’re purchasing a luxury primary residence, refinancing a complex portfolio, or racing the clock on an investment opportunity, Insignia Mortgage is positioned to deliver smarter structures—and better outcomes—in 2026 and beyond. Connect with our team today by calling 310-730-1469 or check out current loan program rates here.

Recent Loan Successes: How Insignia Mortgage Continues Delivering Solutions for Complex Borrower Scenarios

At Insignia Mortgage, we specialize in navigating the most challenging real estate finance situations—from high-LTV jumbo purchases to no-income loans, interest-only structures, and sophisticated investment transactions. Our boutique lending approach, deep lender network, and decades of jumbo and non-QM expertise allow us to deliver fast, flexible, and highly customized financing solutions for clients nationwide.

Below is a highlight of recent loan successes across California and Florida that demonstrate the Insignia difference.

Sherman Oaks, CA — High-LTV Interest-Only Purchase

Loan Amount: $4.175M Program: 7/6 ARM — Interest Only LTV: 79% Rate: 5.50% / 5.63% APR Timeline: < 3.5 weeks

Challenge: A borrower seeking high-LTV, interest-only financing approached Insignia after struggling to find a lender willing to meet their requirements.

Solution: Our team quickly matched the client with a lender offering a competitive interest-only loan at an exceptional rate. The transaction was completed in under 3.5 weeks—ensuring the buyer closed on time and secured the home they wanted.

Challenge: The borrower had no documented income and was in the middle of a divorce, making traditional loan approvals nearly impossible.

Solution: Insignia sourced a lender able to rely on the borrower’s balance sheet—rather than income—to structure an approval. The client closed successfully with a long-term fixed rate solution tailored to their unique financial situation.

Los Angeles, CA — 21-Day Close for 1031 Exchange Investment Property

Loan Amount: $7.5M Program: 5/1 ARM LTV: 50% Rate: 6.37% / 6.30% APR Timeline: 21 days

Challenge: A real estate investor needed to close quickly to complete a 1031 Exchange, leaving no room for delays and requiring a lender who understood complex income.

Solution: Insignia secured a lender offering both speed and competitive pricing. The deal was funded in just 21 days—preserving the client’s exchange timeline and investment strategy.

Los Angeles, CA — High Debt-to-Income Borrower Secures Great Rate

Challenge: The borrower had a high DTI and had already been turned down by several banks.

Solution: Insignia partnered the borrower with a local bank comfortable with their full financial picture, including strong assets. The borrower received an excellent rate and was able to vest the property in an LLC.

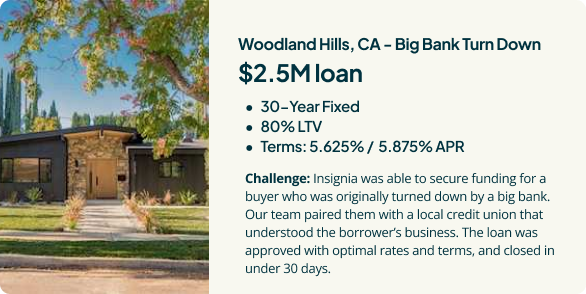

Woodland Hills, CA — Big Bank Turn-Down Turned Fast Approval

Challenge: After being rejected by a major bank, the borrower needed a solution quickly to keep their purchase on track.

Solution: Insignia connected the borrower with a local credit union that understood their unique business structure. The loan was approved with optimal terms and closed in under 30 days.

Montecito, CA — $9.5M Interest-Only Take-Out of Construction Loan

Loan Amount: $9.5M Program: 5/6 ARM — Interest Only Use: Construction take-out Rate: 5.50% / 5.80% APR

Challenge: The borrower needed an interest-only solution to refinance a construction loan on a property still in development.

Solution: Insignia arranged financing through a local private bank offering excellent pricing and fast execution. The client secured long-term flexibility with a smooth, timely close.

Why Borrowers Choose Insignia Mortgage

Across every scenario—no income, complex tax returns, high DTI, fast-close deadlines, or jumbo loan requirements—Insignia Mortgage delivers:

Access to portfolio lenders, private banks, and niche programs unavailable through traditional channels

Fast turn times, even on complex transactions

Customized structuring for foreign nationals, LLC ownership, interest-only needs, and high-net-worth borrowers

Competitive rates on jumbo, non-QM, and specialty loan products

If you have a financing scenario other lenders can’t solve, our team is here to help.

📞 Connect with Insignia Mortgage Call us today at 310-730-1469 to speak with our experienced loan specialists and explore portfolio, jumbo, and non-QM lending options tailored to your needs.

As expected, the Fed lowered rates by 0.25% this week — a move well broadcast by the markets and reflected in the recent drop in both Treasury and mortgage rates. In addition to the movement in rates, what stood out most was the Fed’s accompanying commentary and economic projections. Interestingly, they’re now forecasting slightly higher inflation, steady employment, and modest GDP growth. With that outlook, one might wonder whether a rate cut was even necessary. Still, the Fed made its move, sparking renewed debate about what comes next.

Although some analysts are calling for as many as five rate cuts over the next year, we’re not convinced. Our base case is for two cuts, maybe a third — but that’s far from certain. Inflation remains sticky, and while the labor market isn’t booming, it’s holding up reasonably well. Despite a slowing economy, it’s important to consider the potential impact of Trump-era economic policies, which are just beginning to roll back in and could provide a tailwind in the coming quarters.

One curious development following the Fed announcement was the behavior of the 10-year Treasury. It briefly dipped below 4%, but has since climbed and now sits around 4.12%. This uptick reflects a growing concern among bond pros: when the Fed cuts short-term rates, longer-term yields don’t always follow — and in some cases, they move higher. A large amount of supply is hitting the bond market, with hundreds of billions in Treasuries coming due that need to be refinanced. Add in persistent fiscal deficits and inflation still tracking above target, and you’ve got a recipe for upward pressure on long-term rates.

What This Means for Borrowers

The good news is that lower short-term rates are already providing relief for borrowers with floating-rate loans, HELOCs, or bridge financing tied to short-term benchmarks. For borrowers seeking long-term fixed-rate solutions, the outcome depends on where the 10-year Treasury settles.

For now, we believe the majority of the rate drop has already been priced in. We don’t foresee significantly lower rates from here. That said, public awareness of this move is growing. As expected, our phones have been lighting up with calls for pre-approvals and refinance requests.

Industry Insights on Today’s Housing Market and Creative Lending Solutions

We’re excited to announce that Damon Germanides, co-founder of Insignia Mortgage, was recently featured in Mortgage Professional America (MPA) Magazine — one of the most respected publications in the mortgage and real estate finance industry.

In his interview, Damon shares candid insights on today’s “illiquid” housing market, the impact of historically low rates, and why brokers must lead with honesty when advising clients. He also highlights how creative loan solutions, including bridge financing through Insignia Capital Corp, are helping borrowers and brokers navigate this challenging environment.

Key Takeaways from Damon’s MPA Interview

Why waiting for 2% mortgage rates isn’t realistic Damon explains that the era of ultra-low rates is over and that buyers waiting for them to return may be on the sidelines indefinitely.

The challenges of an illiquid housing market From seniors staying put to first-time buyers unable to move up, Damon outlines why housing supply remains tight and mobility limited.

Why honesty matters in mortgage advising Instead of telling clients “it’s always a great time to buy,” Damon emphasizes the importance of being transparent about market realities — a key to building trust.

Bridge financing as a solution With traditional banks pulling back, Damon discusses how Insignia Capital Corp is providing flexible bridge loans to help clients unlock equity and move forward with confidence.

Why This Feature Matters

Damon’s inclusion in MPA Magazine reinforces Insignia Mortgage’s reputation as a trusted leader in complex lending. With over a decade of experience funding non-QM loans, jumbo financing, and creative real estate solutions, Insignia continues to be a go-to resource for borrowers, real estate agents, and investors navigating California’s luxury markets.

(1) No Tax Return loans and foreign national loan products require other forms of income documentation and asset verification in lieu of tax returns. Not all applicants will qualify. Some products we offer may have a higher interest rate, more points or more fees than other products requiring more extensive or different documentation. (2) Minimum FICO, reserve, and other requirements apply. Contact your loan officer for additional program guidelines, restrictions, and eligibility requirements. Rates, points, APRs and programs are subject to change without notice. Loan to values (LTV) are based on appraised value. Actual closing times will vary based on borrower qualifications and loan terms. All loans are subject to credit approval. (3) With an interest-only mortgage payment, you will not pay down the loan's principal balance during the interest-only period. Once the interest-only period ends, your payments will increase to pay back the principal and interest. Rates are subject to increase over the life of the loan. Contact your Insignia Mortgage, Inc. loan officer to determine what your payments might be once the interest-only period ends. (4) With an adjustable rate mortgage (ARM), once the fixed rate period ends, the loan payment will adjust after an initial period and then adjust on a regular basis as set forth in the loan documents. For example, a “3/1” loan will have an interest adjustment 3 years after the loan closes and every 12 months thereafter. Also, the loan will be subject to annual and lifetime adjustment caps. Contact your Insignia Mortgage loan officer to determine what your payments might be once the fixed rate period of the loan ends. (5) Insignia Mortgage, Inc., is a real estate broker licensed by the CA Department of Real Estate, DRE #01969620, NMLS #1277691

(2) Disclosures

(1) Minimum FICO, reserve, and other requirements apply. Contact your loan officer for additional program guidelines, restrictions, and eligibility requirements. Rates, points, APRs and programs are subject to change without notice. Actual closing times will vary based on borrower qualifications and loan terms. All loans are subject to credit approval. (2) “Loan to Cost” (LTC) is defined as the acquisition price of the property plus the cost to build as determined by a bank appraisal. Contact your loan officer for additional program guidelines, restrictions, and eligibility requirements. (3) With an interest-only mortgage payment, you will not pay down the loan's principal balance during the interest-only period. Once the interest-only period ends, your payments will increase to pay back the principal and interest. Rates are subject to increase over the life of the loan. Contact your Insignia Mortgage, Inc. loan officer to determine what your payments might be once the interest-only period ends. (4) With an adjustable rate mortgage (ARM), the loan payment will adjust after an initial period and then adjust on a regular basis as set forth in the loan documents. For example, a “3/1” loan will have an interest adjustment 3 years after the loan closes and every 12 months thereafter. Also, the loan will be subject to annual and lifetime adjustment caps. Contact your Insignia Mortgage loan officer to determine what your payments might be once the fixed rate period of the loan ends. (5) Insignia Mortgage, Inc., is a real estate broker licensed by the CA Department of Real Estate, DRE #01969620, NMLS #1277691.

Disclosures

(1) Disclosures

(1) No Tax Return loans and foreign national loan products require other forms of income documentation and asset verification in lieu of tax returns. Not all applicants will qualify. Some products we offer may have a higher interest rate, more points or more fees than other products requiring more extensive or different documentation. (2) Minimum FICO, reserve, and other requirements apply. Contact your loan officer for additional program guidelines, restrictions, and eligibility requirements. Rates, points, APRs and programs are subject to change without notice. Loan to values (LTV) are based on appraised value. Actual closing times will vary based on borrower qualifications and loan terms. All loans are subject to credit approval. (3) With an interest-only mortgage payment, you will not pay down the loan's principal balance during the interest-only period. Once the interest-only period ends, your payments will increase to pay back the principal and interest. Rates are subject to increase over the life of the loan. Contact your Insignia Mortgage, Inc. loan officer to determine what your payments might be once the interest-only period ends. (4) With an adjustable rate mortgage (ARM), once the fixed rate period ends, the loan payment will adjust after an initial period and then adjust on a regular basis as set forth in the loan documents. For example, a “3/1” loan will have an interest adjustment 3 years after the loan closes and every 12 months thereafter. Also, the loan will be subject to annual and lifetime adjustment caps. Contact your Insignia Mortgage loan officer to determine what your payments might be once the fixed rate period of the loan ends. (5) Insignia Mortgage, Inc., is a real estate broker licensed by the CA Department of Real Estate, DRE #01969620, NMLS #1277691

(2) Disclosures

(1) Minimum FICO, reserve, and other requirements apply. Contact your loan officer for additional program guidelines, restrictions, and eligibility requirements. Rates, points, APRs and programs are subject to change without notice. Actual closing times will vary based on borrower qualifications and loan terms. All loans are subject to credit approval. (2) “Loan to Cost” (LTC) is defined as the acquisition price of the property plus the cost to build as determined by a bank appraisal. Contact your loan officer for additional program guidelines, restrictions, and eligibility requirements. (3) With an interest-only mortgage payment, you will not pay down the loan's principal balance during the interest-only period. Once the interest-only period ends, your payments will increase to pay back the principal and interest. Rates are subject to increase over the life of the loan. Contact your Insignia Mortgage, Inc. loan officer to determine what your payments might be once the interest-only period ends. (4) With an adjustable rate mortgage (ARM), the loan payment will adjust after an initial period and then adjust on a regular basis as set forth in the loan documents. For example, a “3/1” loan will have an interest adjustment 3 years after the loan closes and every 12 months thereafter. Also, the loan will be subject to annual and lifetime adjustment caps. Contact your Insignia Mortgage loan officer to determine what your payments might be once the fixed rate period of the loan ends. (5) Insignia Mortgage, Inc., is a real estate broker licensed by the CA Department of Real Estate, DRE #01969620, NMLS #1277691.

Disclosure

Insignia Mortgage corporate NMLS #1277691 and DRE #01969620