Mortgage Rates Edge Higher: What It Means for the Real Estate Market

Mortgage rates have edged higher as the economy remains resilient, while concerns over a potential rise in inflation linger. Consumer sentiment has improved, proving that the US consumer is tenacious, if nothing else. Nonetheless, credit card and auto loans have risen as consumers continue to feel the pressures of cumulative inflation. Housing activity, which is sensitive to interest rates, has started to stall as mortgage rates have moved up, causing prospective buyers to wait for a better entry point. Home builders are continuing to offer major incentives to buyers to move product and create buzz. If rates move further, we fully expect to see 2-1 buydowns and other incentives being mentioned in the Wall Street Journal as ways to attract prospective buyers. Lennar, a major home builder, recently disclosed that the buydowns and incentives combined amount up to $48,000 per home. That is a big number, especially since the average home Lennar sells costs $422,000.

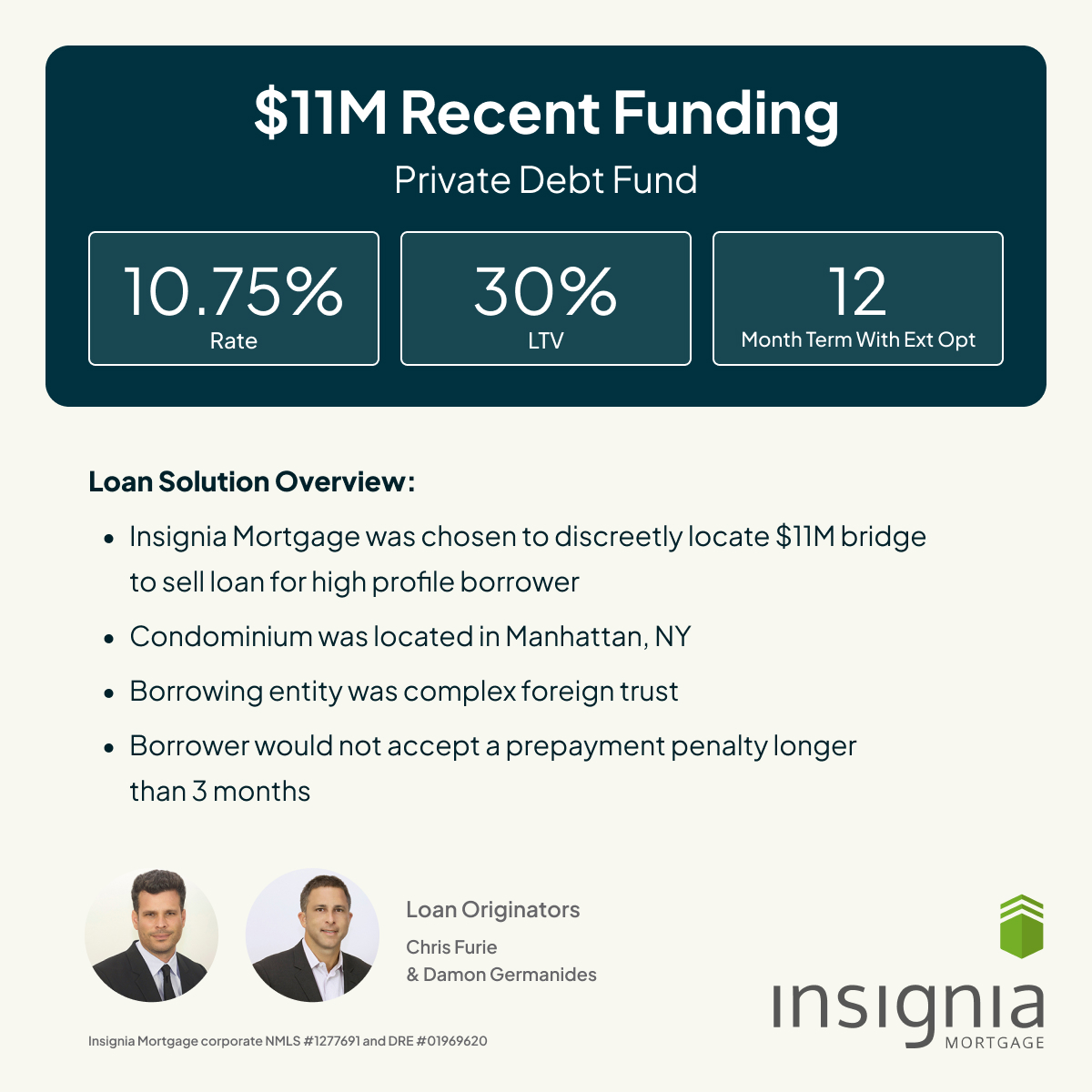

There is still a silver lining, particularly for high-net-worth borrowers. Banks are still competing for top-tier clients, and those who qualify for private banking can secure loans in the mid-5% range. This is positive news for the luxury real estate market. Also, some smaller banks are looking at borrower financials more holistically and making commonsense decisions for borrowers with means. For first-time or lower-end borrowers, banks are offering very attractive terms to meet community lending requirements, including loans up to 100% financing with no points or mortgage insurance. These types of loans cap out at around $1M.

Some very respected Wall Street traders have opined as of late on the potential mistake the Fed made by cutting rates by 50 basis points. Their concern is centered around a good overall U.S. economy, low unemployment, and the return of animal spirits to the market as a result of the recent cut in interest rates. With US equities near or at all-time highs, Bitcoin and other speculative asset classes have soared. Credit spreads are tight and money seems abundant within the financial system. For those borrowers not in real estate or other industries heavily reliant on debt, there has been less pain than imagined from the initial Fed hikes. The big concern is if the Fed eases too quickly, that inflation will kick back up and they will be forced to raise interest rates again. This would be a very bad outcome for the respectability of the Federal Reserve. Next month brings both a Presidential election and a Fed meeting, both events that we will be watching closely.