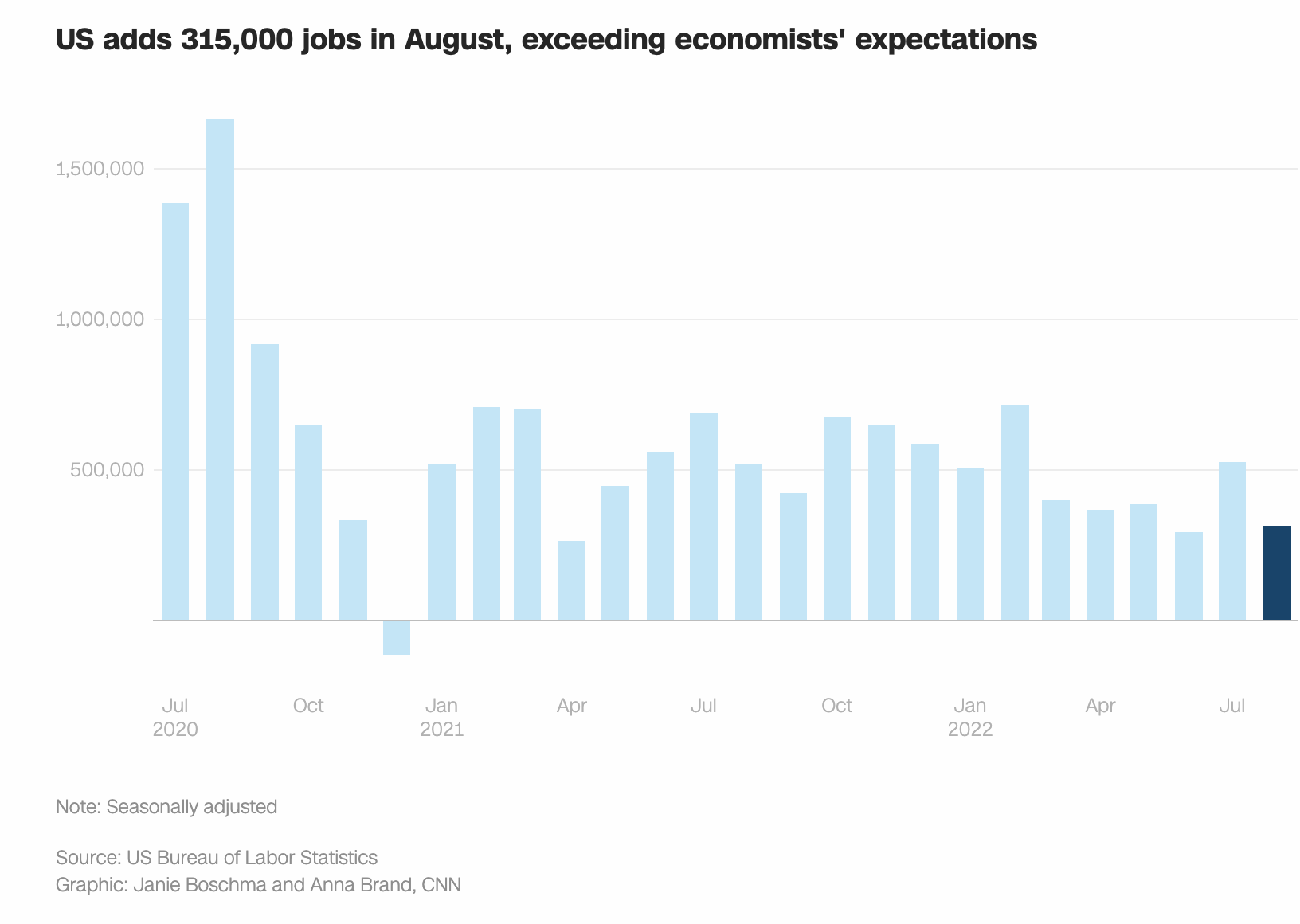

Equity Markets Move Higher, Encouraging Soft Landing For The Economy

U.S. equity markets proved resilient against the backdrop of a Hawkish Federal Reserve. Several voting members of the Fed spoke this week and the message was clear: short-term interest rates are going higher to combat inflation. The Fed wants input inflation to go down (think wages and energy) as well as consumption (think feeling poorer due to home value or retirement accounts being down). However, the equity markets didn’t get the memo and rallied into the weekend.

Markets can sometimes react in a way that may seem irrational initially, but over time proves correct. In my mind, the equity rally suggests inflation may be coming down and job destruction may be happening more quickly. The so-called soft landing for the economy will be the result of Fed tightening. My prediction is there is more pain ahead. Volatile markets both up and down will be the norm for the balance of the year. The Fed will err on the side of higher interest rates for longer, which will put continued pressure on bonds and all investable assets. Remember, it takes time for the Fed’s policies to work their way into the system. That is why caution in this type of environment is so important. Don’t fight the Fed.

75 bp seems to be the likely direction in short-term interest rates when the Fed meets later this month. That number was forecasted to the Wall Street Journal to help mitigate any surprises. The cost of debt is rising quickly. Higher yields are becoming attractive for savers, which is one positive to this so-called “return to normal interest rate” journey central bankers are taking us on. Real estate prices are adjusting as expected in the face of higher interest-carrying costs. Buyer and seller negotiating is back in vogue and all offers are being looked at.

One interesting phenomenon that’s presented itself has me particularly excited to share. This past week Insignia Mortgage has located three new lending sources which specialize in the following: (1) financing high-net-worth domestic or foreign borrowers, (2) a new regional bank that offers attractive interest-only jumbo loans, and (3) a new commercial bank that offers investment property loans up to 20 million dollars. As rates have increased, so has the appetite to lend for those banks that didn’t chase yield to near zero. While business remains challenging, all is not lost in this wonderful free market economy we get to live in.